If you owe back taxes, your balance steadily grows each month that it remains unpaid. After the filing deadline has passed, the IRS will begin to charge both penalties and interest on the amount owed. These charges can make a difficult situation much worse.

The IRS stops charging penalties and interest only after you have resolved your tax debt permanently, or the entire tax debt is forgiven.

Penalties

Below, I will detail the two types of penalties charged on tax debt.

- Late Payment Penalty: If you don’t pay what you owe upon filing your return, you will be charged a penalty. The late-payment penalty is one-half of one percent of the tax owed for each month it is unpaid. Every month you owe, the penalty amount increases by a half of a percent. So the first month the IRS will charge you a half percent of the tax due, the second month 1%, the third month 1.5%, etc. The late-payment penalty does max out at 25%. Be mindful that filing an extension does not extend the payment due date.

- Failure-To-File: The failure-to-file penalty is generally more than the failure-to-pay penalty. If you are required to file a return, and you do not file, then the IRS charges a failure-to-file penalty. Just like the late-payment penalty, this penalty escalates every month, but faster. The late-filing penalty starts out at five percent (5%) of the tax owed for each month your return is late. The penalty will increase by 5% every month for a maximum of five months, hitting a maximum limit of 25% in the fifth month your return is late.

When both penalties run concurrently, the late-filing penalty is reduced from 5% to 4 1/2% monthly. When both penalties apply, the late-filing penalty hits its max at 22.5%, with the late-payment still maxing out at 25%.

The combined penalty for not paying on time and not filing on time: 47.5%. This does not include interest!

Interest

In addition to penalties, the IRS also charges interest on tax debt. The interest is charged at the federal short-term rate plus 3% for a year. It is compounded daily and does not include payment extensions.

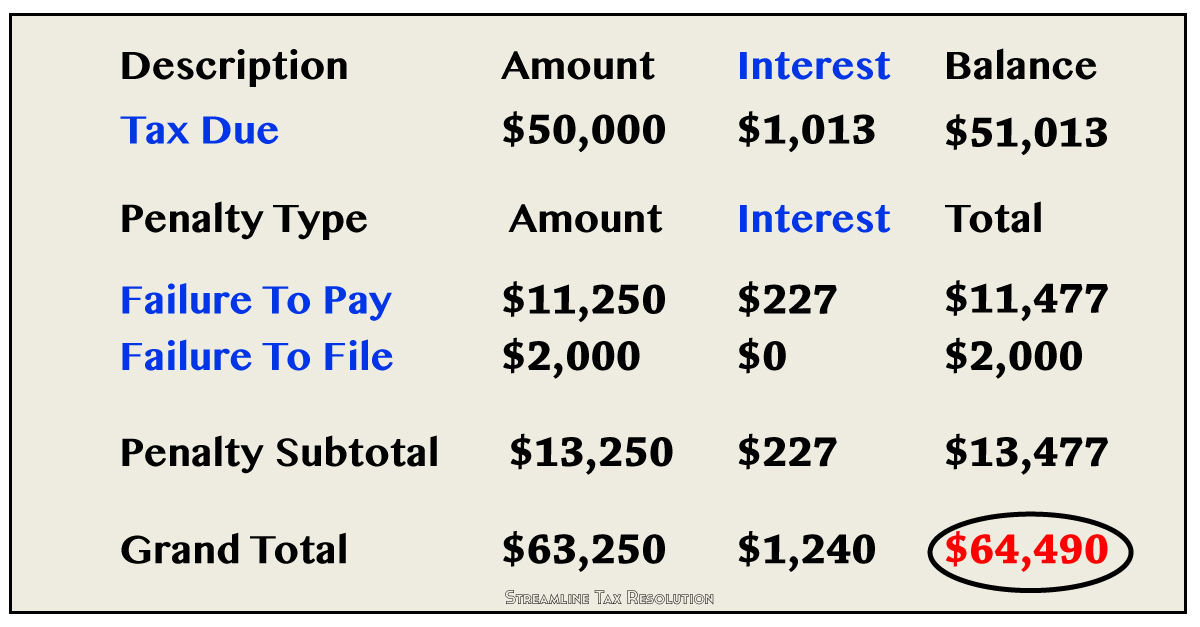

For example, if you filed your return 8 months late, and owed $50,000 on the return,

you could eventually owe an additional $13,477 in penalties. As for interest, you are looking at incurring $1,240 tacked onto both the outstanding balance & the penalty for failure to pay. In total, your tax bill increased by $14,490. That’s nearly a 30% increase in only 8 months! YIKES!! (Please note these numbers are estimates only – you get the idea.)

What If You Can’t Pay Your Taxes On Time?

To avoid paying more in penalties and interest, you should make efforts to resolve your tax debt today. If you are struggling with handling your tax issues , contact a tax resolution specialist immediately. By doing so, you will have taken the first step in protecting your assets from levy/garnishment action. A resolution specialist will also help you strategize the best method possible to put and end to your tax problems, allowing you to move on with your life.