Craig Thomas

Latest posts by Craig Thomas (see all)

- Chris Feels Victorious - September 8, 2016

- Are You At Risk of a Levy? - May 26, 2016

- 3 Ways To Survive Your Spouse’s Tax Troubles - February 15, 2016

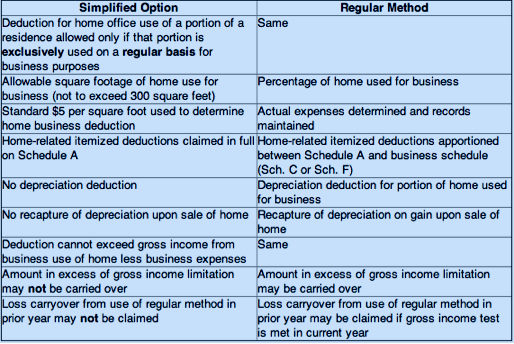

For many of those who work from home, the process of calculating home-office deductions can be confusing. That’s why, beginning last filing season, the IRS has offered a simplified alternative option to calculate home-office itemized deductions.

Under the old method, taxpayers labored to complete a very intricate and drawn-out IRS form. The majority of time was spent on allocating expenses between personal use, and business use, which could took all day if you were not organized. The percentage of your home devoted to business also had to be determined.

Under the new optional method, you can simply claim $5 per square foot of space, which meets the definition of a qualified home office, up to a maximum of 300 square feet. Therefore, the maximum amount that can be deducted using this method is $1,500.

Besides saving time, this simplified option can significantly reduce the burden of record-keeping by allowing a taxpayer to use a flat rate for the allowable square footage of the office, rather than determine actual expenses.

For the most part, you can continue to take the same allowable home-related deductions under the new method, but there are a couple of changes in the criteria for eligibility in taking certain deductions under the simplified method, such as depreciation.

The IRS table below shows the comparisons of the two methods:

Whether or not the new simplified method works to your advantage, it’s good to see that the IRS has actually made something ‘easier’.

For more information on tax resolution services,visit: www.streamlinetaxresolution.com

Craig Thomas can be reached at: cthomas@streamlinetaxresolution.com

Related Posts

5 Tips You Should Know about Employee Business Expenses

5 Tips You Should Know about Employee Business Expenses 15 Ways To Avoid The Jaws Of The IRS Auditor

15 Ways To Avoid The Jaws Of The IRS Auditor How To Save Money And Make Life Easier Come Tax Time

How To Save Money And Make Life Easier Come Tax Time Employee vs. Independent Contractor: The Common Tax Mistake That Can Cost Your Business

Employee vs. Independent Contractor: The Common Tax Mistake That Can Cost Your Business IRS Levy

IRS Levy How I Turned My Friend’s Tax Trouble Into a $25k Savings

How I Turned My Friend’s Tax Trouble Into a $25k Savings